Вопросы без ответа

Ситуация становится еще более запутанной, когда задаешься вопросом, почему банки будут платить Apple за транзакцию, если подход Google им ничего не стоит. Возможно, Apple удалось убедить их, что ее пользователи будут делать больше покупок с помощью Apple Pay, или, возможно, банки считают, что они получают эксклюзивное преимущество перед банками, не являющимися партнерами Apple. Или, может быть, Apple просто намного лучше, чем Google, справляется с координацией различных заинтересованных сторон, вовлеченных в такую сложную и запутанную сеть.

Но, несмотря на значительное влияние Apple, с Merchant Customer Exchange (MCX), который включает, среди прочего, Rite Aid ( не будут использовать Apple Pay или Google Wallet.. Вместо этого они работают над своей собственной альтернативой CurrentC, которая сэкономит им значительные суммы денег, взимая плату с банковского счета клиента напрямую, вместо того, чтобы платить комиссию за транзакцию таким платежным системам, как VISA ( V ) и MasterCard ( MA ).

Ни Google, ни Apple не предлагают многого поставщикам за внедрение их систем; хотя на данный момент система CurrentC очень неуклюжая, требуя от пользователя сфотографировать QR-код для оплаты, что делает ее успешное привлечение потребителей маловероятным.

Купить специальный кошелек для смартфона

В 2020 году Apple представила серию iPhone 12, одной из особенностей устройств было наличие магнита на задней панели и поддержка технологии беспроводной зарядки MagSafe. Также компания выпустила несколько аксессуаров, которые можно крепить на «спинку» iPhone — например, MagSafe Wallet, кошелек для хранения банковских карт и пропусков.

Кошелек не очень удобный — он может отвалиться, когда кладешь смартфон в карман. Также из-за отсутствия магнитов аксессуар не очень хорошо держится на iPhone 11 и более старых смартфонах. Однако эта штука позволяет носить карточки рядом с телефоном и быстро извлекать их для оплаты.

Оригинальный кошелек от Apple стоит довольно дорого — больше 5-6 тысяч рублей. К счастью, на AliExpress и других подобных площадках можно приобрести дешевую копию за 300-500 рублей (ищите по запросу MagSafe Wallet). В комплекте к некоторым из них даже кладут магнитное кольцо, которое можно приклеить на заднюю панель iPhone без MagSafe.

Visa, Mastercard, «Мир»: есть ли сейчас разница?

Все три платёжные системы продолжают работать на территории России в обычном режиме — даже если карта выпущена в банке, на который распространяются ограничения. Пользоваться такими картами внутри страны можно, пока у них не истечёт срок действия. Однако многие российские банки пошли навстречу клиентам и продлили его. А некоторые банки и вовсе сделали свои карты бессрочными. Например, так поступил МТС Банк.Пользоваться картами Visa и Mastercard в поездках за границу, если их выпустил любой российский банк, теперь не получится. Если вы планируете такую поездку, заранее позаботьтесь об альтернативных вариантах расчётов и возьмите с собой наличные в подходящей валюте.Карт «Мир» изменения не коснулись: их как и раньше принимают без ограничений на территории России, также в некоторых странах: Турции, Армении, Белоруссии, Таджикистане, Казахстане и других. Полный их список вы найдёте здесь.

What is contactless payment?

Before we dive into Apple Pay and Google Pay, it’s important to understand the technology behind these payment methods. Both operate on contactless payment.

With contactless payment, you don’t need to slide your card at the point of sale (POS) terminal. Instead, you use your card in a compatible device.

Contactless payment uses near field communication (NFC) technology to obtain payments from your device. These terminals use radio frequency identification (RFID) to communicate the payment between the mobile device and the payment reader. The information transmits through RFID to make your payment at the register.

Most people use their mobile phones or compatible wearable devices like watches to make payments. When you get to the register, you simply open the Apple Pay or Google Pay app, hold or wave your device over the POS terminal, and make your payment. It’s a simple process that takes less time than swiping your bank card.

На Ямале заработал Apple Pay?

В ролике наглядно прослеживается процесс заказа в приложении компании:

- пользователь выбирает пиццу и кладет ее в корзину;

- нажимает «оформить заказ»;

- выбирает способ оплаты «Эпл Пей»;

- нажимает «оплатить».

То есть, получается что, формально в этой пиццерии на Ямале можно рассчитываться иностранной мобильной платежной системой, которая на сегодняшний день приостановила деятельность на территории РФ.

Но, без накладок, конечно, не обошлось. Пиццу так и не доставили клиенту, так как ресторан не получил оплату. Заказ аннулировали. Таким образом, смысла от того, что Эпл Пей формально работает на Ямале, никакого нет.

Apple Pay

Apple Pay – which Apple says 85% of U.S. retailers accept – offers a similarly easy, secure and private electronic payment service using iPhone, iPad, Apple Watch or Mac. In addition to an Apple device, all Apple Pay requires is the latest version of iOS, watchOS, or macOS; Apple’s Wallet app; and an Apple ID signed in to iCloud.

How to use Apple Pay

Start using Apple Pay as soon as you add your credit, debit or prepaid cards to your Apple Wallet on any iOS device. Apple Pay is compatible with most credit cards and U.S. banks.

In-store, use Apple Pay on your iPhone or Apple Watch at merchants with a compatible checkout card reader. On the web (in Safari), use your iPhone, iPad or Mac to pay with Apple Pay. Loyalty points, rewards and benefits from your cards continue to accrue when you use Apple Pay.

You can also send or receive money from your iPhone, iPad or Apple Watch. Send money in Messages or ask Siri to pay someone using the credit and debit cards you have stored in Wallet. The money you receive is added to the Apple Pay Cash card in Wallet, so it’s ready to use right away. You can also transfer money in your Apple Pay Cash card to your bank account.

Use Apple Pay to quickly pay friends, but the credit card you choose may charge you a fee for this. Apple doesn’t charge a fee to merchants or consumers.

Apple Pay availability

Devices capable of using Apple Pay within iOS apps or on the web are those with Face ID or Touch ID (except the iPhone 5s):

- iPhone 6 and newer

- iPad Mini 3 and newer

- iPad Air 2 and newer

- iPad (fifth generation and newer)

- iPad Pro

- Apple Watch (first generation and newer)

With 85% of U.S. retailers accepting Apple Pay, it’s not hard to find a merchant where you can shop with Apple Pay. The bigger names include Ace Hardware, Best Buy, Champs, CVS, Firehouse Subs, Foot Locker, Gap, KFC, JetBlue, PetSmart, QuikTrip, Starbucks, Target, Trader Joe’s, Walgreens, Wegmans and White Castle.

Apps and websites that accept Apple Pay include Chipotle, Etsy, Jet, Lyft, MLB.com, Seamless, Staples and Ticketmaster. You can even use Apple Pay to donate to various charities, such as American Red Cross, Feeding America, St. Jude Children’s Research Hospital, and UNICEF, or for mass transit systems.

Apple Pay security

When you make a purchase with Apple Pay, your receipts are kept in your Wallet app, but the transaction information isn’t stored elsewhere. Every transaction you make on your iPhone, iPad or Mac requires authentication with Face ID, Touch ID or your passcode. Your Apple Watch is protected by its unique passcode. If your Apple device is lost or stolen, you can suspend or permanently remove the ability to pay from that device.

When you make an in-store purchase, card numbers and identity credentials aren’t shared with merchants, and your actual card numbers aren’t stored on the Apple device or Apple servers.

Почему не работает мобильное приложение банка?

Мобильные приложения и онлайн-сервисы банков, на которые не распространяются санкции, доступны и на территории России, и за границей — никакие ограничения на их корректную работу не влияют. Проблемы могут возникнуть с приложениями банков на платформе iOS — но только тех, которые попали под действие санкций. Также учтите, что онлайн-сервисы банков сейчас испытывают непривычную нагрузку. В некоторых случаях может возникать ошибка с входом или отдельными операциями. Банки просят относиться к ситуации с пониманием: не паниковать и повторить попытку через несколько минут.

Материал по теме

Как мошенники ловят нас: беспокойство за близких, угроза потери денег, громкие события и другие наживки

Отличаются ли системы между собой?

Безопасность во всех сервисах, прежде всего, обеспечивает токенизация. После добавления в соответствующее приложение банковской карточки создается уникальный виртуальный номер. Ее фактические данные не поступают в торговую точку при оплате.

Системы дают возможность применять бесконтактную оплату не только с телефона. Платежи можно совершать с таких устройств:

- Apple: iPad, Apple Watch, Mac (для покупок в режиме онлайн).

- Google Pay: может применяться на некоторых умных часах на ОС Android Wear.

- Samsung Pay: часы Gear Sport, S2 и S3.

Прямые переводы P2P между двумя пользователями поддерживаются лишь Google и Apple pay. Таким образом, каждая из систем имеет характерные особенности, плюсы и минусы, хотя работают они по идентичному принципу.

Samsung Pay или Google Pay — что лучше?

Возможно, вам, как владельцу Андроид-гаджета, уже приходилось пользоваться подобной системой от Samsung. И перед вами встали вопросы: что лучше, Samsung Pay или Google Pay и стоит ли переходить с одного на другое?

Выбор платежной системы диктуется личным вкусом, но есть факторы, которые играют более значащую роль. Например:

Словом, у того и другого есть и плюсы, и минусы. И что для вас лучше, решать, конечно же, вам. Подключайте и сравнивайте.

Поменять кошелек на телефон или даже часы – неплохое решение, которое сулит удобства. Вместо того чтобы считать наличные или вводить код от карты, достаточно просто поднести смартфон к платежному терминалу.

Самые продвинутые платежные системы – от Google, Samsung и Apple. Впрочем, некоторые бренды типа Garmin и Fitbit также создают свои «платежки», но они слабо распространены и в большинстве странах недоступны.

Итак, каковы различия между платежными популярными платежными системами?

Что касается автономных платежей, то они поддерживаются на всех трех системах, и если у вас нет сигнала или Wi-Fi, то производит оплату все равно можно, правда, число транзакций ограничено.

Теория взлома

В этой бочке меда нашлась ложка дегтя. Как бы ни старались разработчики, в сервисе Apple Pay есть проблемные места. И это во многом зависит не от Apple. В процессе движения средств задействованы многие другие структуры, в том числе банки с их огромными пробелами в безопасности.

Сканер отпечатков пальцев не всегда работает корректно. Предоставляя современное и, казалось бы, надежное средство удостоверения личности, оно одновременно является огромной дырой в безопасности. Если Touch ID выйдет из строя, можно воспользоваться пин-кодом. Это сводит на нет всю продвинутую безопасность.

Пин-код можно подглядеть, спутать, нажать не те клавиши, короче, человеческий фактор в действии. При оплате с помощью часов Apple Watch отпечаток не требуется, в этом случае вопрос о безопасности встаёт острее.

В связи с этим появились дополнительные инструменты проверки: секретный код, одноразовый пароль, звонок в службу поддержки клиентов или предоставление информации о предыдущих покупках.

Некоторые банки в других странах требуют от пользователя авторизации в мобильном интернет-банкинге. Эти действия уменьшают удобство использования Apple Pay из-за появления дополнительных уровней проверки.

На данный момент в России работает самый простой формат оплаты без дополнительных авторизаций в процессе.

Между тем, Apple Pay по-прежнему не взломана.

Для чего нужен Apple Pay?

Приложение позволяет не только быстро и без дополнительных кодов подтверждения оплачивать услуги различных компаний, но и хранить данные по всем своим картам в единой программе.

Оплата услуг и прочие функции приложения (информация на официальном сайте)

Оплата услуг и прочие функции приложения (информация на официальном сайте)

Иными словами, при использовании приложения не требуется дополнительно носить с собой кредитные и другие карты, а также дополнительно защищать свои платежные данные от несанкционированного доступа.

Хранить можно самые различные карты, а также купоны и скидочные карты, но и такие документы, как билеты, покупочные купоны, подарочные купоны и многое другое.

Особенно удобно данное приложение для тех, кто постоянно путешествует, совершает множество покупок в различных торговых точках, а также активно пользуется услугами различных компаний и заведений.

Pros and cons of mobile wallets

Mobile wallets are convenient, but they’re not a perfect payment solution. Here’s a look at their pros and cons.

Pros of mobile wallets

- They’re easy to use. Mobile wallets are easy to install on your phone and use for purchases. If your device is relatively new and has NFC-enabled features, you won’t have any trouble in the checkout line.

- They’re more secure than you’d think. Google Pay, Apple Pay and Samsung Pay are built with security in mind. All three platforms hide your personal information and credit card numbers from merchants, and they require you to sign in to your device.

- You don’t need to carry credit cards. One of the main advantages of mobile wallets is that you can leave your credit cards at home (mostly). As long as you frequent supermarkets and stores that accept mobile wallet payments, you carry all your cards on your device.

- They have great rewards programs. Google, Apple and Samsung frequently roll out new promotion and reward programs to keep shop-savvy consumers on their platforms.

Cons of mobile wallets

- They are not universally accepted. While mobile wallets are convenient where they are accepted, it’s still a good idea to keep a credit card or extra cash on hand just in case.

- You may have data privacy concerns. Even though mobile wallet platforms are very secure, they still have the potential to gather and record your transaction history.

- They are dependent on your phone. The greatest disadvantage of a mobile wallet platform is that it’s directly tied to your phone, making your phone the single point of failure. If your battery dies or you lose your phone and don’t have your wallet on hand, you’ll be stuck with no payment method while you’re on the go.

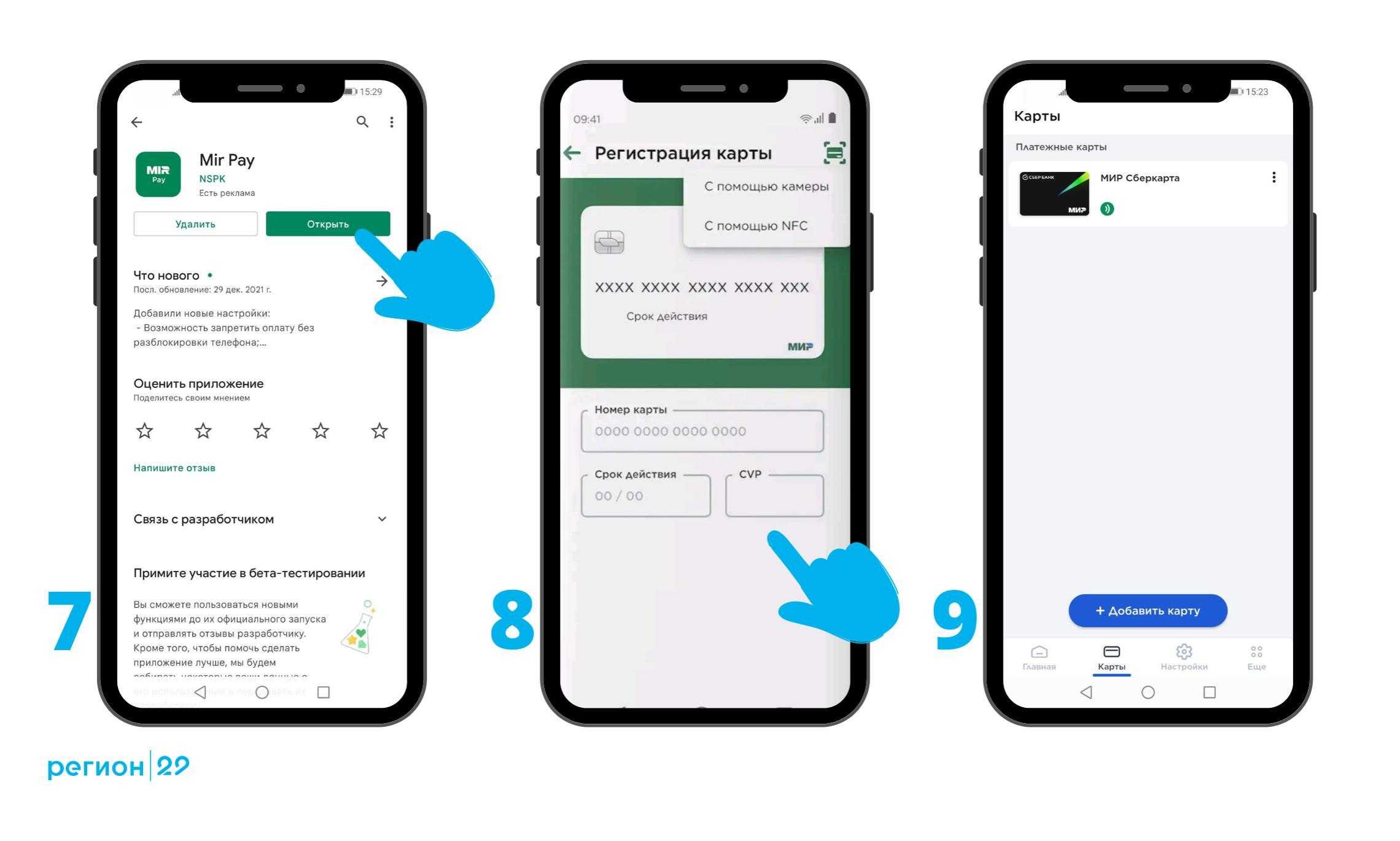

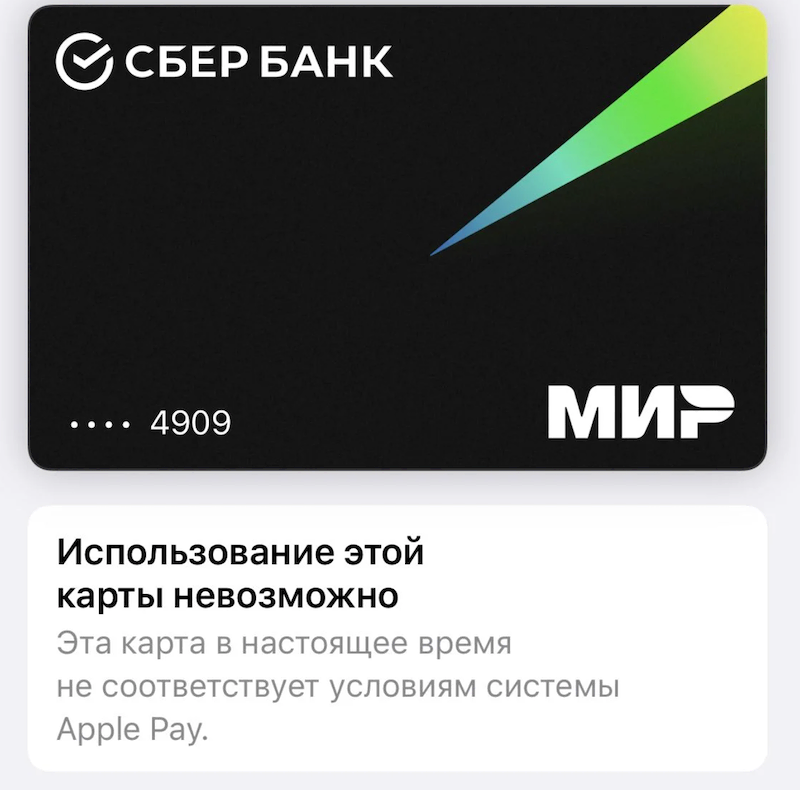

Можно ли подключить Apple Pay в России?

Привычным способом это сделать нельзя — при попытке добавить любую карту, выпущенную российским банком, сервис выдает ошибку. Ранее добавленные карты не работают — под каждым виртуальным пластиком висит плашка, что использование данной карты невозможно.

11 апреля в сети нашли способ добавления российских карт в сервис Apple Pay. Метод работает, но спустя несколько часов сервис блокирует пластик.

- Заходим с компьютера на сайт icloud.com/find, вводим пароль Apple ID

- Находим в списке гаджетов свой iPhone и переводим его в режим пропажи

- На iPhone вводим цифровой пароль, также вводим пароль от Apple ID

- В Apple Pay появятся работающие карты

Why the slow adoption rates?

According to data from PYMNTS, Apple Pay is leading the digital wallet adoption race, but it’s ahead in a very slowly growing market, where only 4.5% of users report using a mobile wallet for an in-store purchase in 2021.

In 2021, 44% of eligible iPhones were equipped with Apple Pay, but only 1.7% actually used Apple Pay for in-store purchases – down from 3% in 2017. Usage rates for Google Pay and Samsung Pay are even lower.

Mobile payment platforms offer greater convenience, speed and security over conventional payment methods, and they’re widely accepted and available, so why are they struggling to gain widespread adoption?

There are a few major barriers to adoption that have stymied consumer demand and slowed merchant incentives to adopt the necessary infrastructure to spur further adoption.

-

Preference for contactless debit and credit cards: Before the COVID-19 pandemic, many people were unfamiliar with the concept of contactless payments. Since the pandemic, however, contactless payments with debit and credit cards have become routine.

Contactless credit and debit card payments have many of the same in-store advantages as digital wallets, offering a touch-free checkout experience and convenience, and consumers often choose this payment method.

- Inconsistent infrastructure: Even though NFC payment-equipped POS systems are much more commonplace, many merchants aren’t there yet. When NFC support is more readily available, consumers may utilize the payment platforms more.

- Ingrained habits: Most U.S. consumers are perfectly comfortable paying with credit and debit cards, particularly with pandemic-induced contactless debit and credit card transactions. Many people haven’t used digital wallets or NFC-enabled POS systems, and these systems can differ from store to store and terminal to terminal.

However, as digital wallet payments become more widespread, more consumers will grow accustomed to them. The most promising signs for contactless payment adoption come from younger consumers, suggesting that demand will grow as more consumers age into the market.

Venmo

Venmo has grown a lot more popular over the past few years, becoming the preferred way for many people to transfer cash to their friends. In fact, Venmo has become a verb — “Venmo me!” After creating your account, you’ll be asked to add people to your friends list, which makes it easier to transfer money the next time you need to do so.

There are a few things to keep in mind when using Venmo, however. For example, the team behind it has tried to make the service highly social, which may frustrate some. When you send money, you’ll have the option to make the transaction public, and while you most likely don’t want or need to do this, you’ll have to be careful to not accidentally select the wrong option.

Like other services, when someone sends you money, it sits in your Venmo account — it can be sent to others or transferred to your bank account by “checking out.” It’s free to use Venmo with a debit card. It will still cost you 3% to use a credit card, but if you’re not too fond of linking a service to your bank account, it might be nice for you to not have to pay a fee for each transaction. Not only that, but Venmo says that money will be transferred to your bank account within one business day, which is pretty quick — or you can pay a 1% fee (max $10) for an instant transfer. Venmo recently added an option to instantly send money to your debit card for 25 cents; there’s still a free option, but it’s not as fast.

Venmo also offers a credit card that gives you up to 3% cashback on your purchases and a debit card which offers a similar cashback feature. You can even scan physical checks directly into your Venmo account with the Cash A Check feature, and be paid your salary via Direct Deposit.

Venmo is obviously meant to be used for everyday transactions, and as such, it sets a weekly limit of just under $5,000. It’s still a lot of money, sure, but you won’t be using Venmo to send a huge amount of cash like Apple Pay Cash or PayPal.

Android iOS

Apple Pay vs Google Pay: Similarities

Though they’re direct competitors, Apple Pay and Google Pay are similar apps that enable peer-to-peer, in-person, and online payments. They both allow customers to upload debit, prepaid, credit, and rewards card information and use near-field communication (NFC) to make contactless payments by tapping a device to a reader.

With these apps, your customers can quickly and efficiently check out with just a single tap on a screen — instead of physically touching your payment terminal or revealing any card numbers. Apple Pay and Google Pay make online purchases convenient, too, thanks to pre-populated fields and PIN or Touch ID verification.

Безопасность

Мошенничество с кредитными картами было серьезной проблемой в США. Поскольку банки и розничные торговцы работают над обновлением своих платформ, мобильные платежные системы, такие как Pay и Wallet, могут фактически позволить США вырваться на передний край безопасности платежей.

Хотя обе системы кажутся одинаково надежными, обе компании используют разные подходы, определяющие, что их продукты могут и не могут. Для потребителя использование Touch ID и аутентификации по PIN-коду является наиболее заметной разницей, но за кулисами происходит гораздо больше. Наиболее важным является тот факт, что ни одна из систем не раскрывает продавцу реквизиты карты пользователя.

В обеих системах данные карты пользователя предоставляются только один раз во время начальной настройки. Google берет на себя роль посредника и сохраняет данные вашей карты на своих серверах. Затем они выдают на ваше устройство виртуальную карту — виртуальную карту Google Кошелька. При оплате устройство передает только эту виртуальную карту. Продавец никогда не видит вашу настоящую карту, которая надежно защищена собственными защищенными серверами Google. Когда продавец снимает оплату с виртуальной карты, Google, в свою очередь, снимает средства с вашей сохраненной дебетовой или кредитной карты, будучи единственным лицом, которое когда-либо видит вашу реальную карту во время этой транзакции.

Apple использует другую систему, известную как токенизация. Здесь, когда данные вашей карты предоставляются устройству, оно напрямую связывается с банком-эмитентом и после подтверждения получает специальный токен устройства и карты, называемый номером учетной записи устройства (DAN), который хранится на защищенном чипе на устройстве. DAN структурно напоминает номер кредитной карты и передается продавцу при совершении любого платежа и авторизуется в банке обычным способом.

Достоинства Apple Pay

- Нет необходимости постоянно иметь при себе карту или деньги.

- Все операции выполняются с помощью гаджета.

- Все покупки можно объединить в один отчет, даже если они были сделаны посредством разных банковских карт.

- В ближайшем будущем сервис откроет доступ к оформлению кредита.

- Возможность отслеживания всех затрат с целью их оптимизации.

- Безопасность сервиса на высоком уровне, несанкционированное вмешательство в работу практически исключено.

- В случае утери телефона данные сервиса будут недоступны для злоумышленников.

- Совершение платежей упрощено, не требуется проводить сложные операции.

- Покупка посредством сервиса Apple Pay ускоряет движение живой очереди, так как от покупателя требуется лишь прислонить гаджет к терминалу. Не нужно ждать сдачи, вводить пин-код.

- Мобильное устройство упрощает жизнь, ведь карту можно потерять, а ее восстановление затруднительно и требует много времени.

Где можно скачать Apple Pay?

Скачать приложение можно на официальных источниках компании, например, на сайте Apple или же на ресурсе Google Play.

Схема подключения и работы платежной системы

Схема подключения и работы платежной системы

На сегодняшний день приложение предоставляется для скачивания и использования бесплатно – никаких дополнительных сборов и взысканий быть не может.

Если вам предлагают скачать приложение платно или же заплатить за его использование, вероятнее всего вы связались с мошенниками и вам следует более надежный источник для скачивания.

Сразу после скачивания пользователь может установить приложение и начать его использовать в удобное для себя время.

Cash App

Next up on our list is Cash App, built by Square, which is perhaps best known for its point-of-sale systems for the iPad and iPhone. At first glance, you might have trouble seeing why you would want to opt for Cash App over other services, but it does have one unique selling point — you don’t have to set up an account to use it. However, you will need to verify your identity to lift the spending limit of $1,000 within any 30-day period. On the plus side, Cash App charges no fees to send or receive payments in the U.S. or abroad — although the current exchange rate applies for international payments. You’ll pay a 3% fee for all credit card payments.

You can also order a debit card with Cash App. The virtual card can be used for online purchases — iOS users can link the card to Apple Pay — and you’ll also receive a physical card that you can use to make in-store payments.

![Как использовать google pay на iphone, ipad [2021 updated] - wapk](https://befam.ru/wp-content/uploads/3/e/2/3e2dce633723d16bcfe58a3e1027f724.png)

Android iOS

Security Systems

Credit card fraud remains a significant problem worldwide. As banks and retailers work to upgrade their platforms, mobile payment systems like Apple Pay and Google Wallet may allow the U.S. to leapfrog to the forefront of payment security.

Though the two systems appear to be equally robust, the companies take different approaches that shape what their products can and can’t do. For the consumer, the use of Touch ID versus personal identification (PIN) authentication is the most visible difference, but behind the scenes, there is a lot more happening. Most important is the fact that neither system reveals the user’s card details to the vendor.

Google Security

With both systems, you provide your card details only once, during the initial setup. Google adopts an intermediary role and saves your card details on its servers. It then issues a virtual card to your device, the Google Pay virtual card.

When paying, the device only transmits the Google Pay virtual card’s information. The vendor never sees your real card, which is protected by Google’s secure servers.

When the seller charges the virtual card, Google, in turn, charges your stored debit or credit card and is the only entity that ever sees your real card through this transaction.

Apple Security

Apple employs a different system known as tokenization. Here, when your card details are provided to the device, it contacts the issuing bank directly and, upon confirmation, receives a device- and card-specific token called the Device Account Number (DAN), which is stored on a secure chip on the device. The DAN structurally resembles a credit card number and is passed on to the merchant when any payment is made before getting authorized by the bank.

Does Apple Pay Charge Fees?

No, Apple Pay doesn’t charge consumers fees. Instead, it makes money directly from the bank that issued the card linked to the Apple Pay account.

Does Google Wallet Charge Fees?

No, Google Wallet doesn’t charge consumers fees. Google makes money by charging vendors a percentage of each transaction, as well as through targeted ads.

What’s the best mobile payment app?

Apple Pay, Google Pay and Samsung Pay are popular options compatible with many merchant card readers, credit cards and banks. Other options include Chase Pay, MasterCard PayPass, PayPal and Visa Checkout.

While all these platforms serve virtually the same function, each is slightly different, with its strengths and weaknesses. Despite slow adoption, the best point-of-sale (POS) systems support these mobile payment platforms as more merchants allow for NFC-enabled payments.

We’ll take a look at the three top mobile wallets, how they work, and what consumers and entrepreneurs can expect in terms of more widespread adoption.

Что можно оплатить?

При помощи Эпл Пэй можно оплатить любые товары и услуги в обычных торговых точках и в сети Интернет. Ограничен список таких платежных заведений исключительно списком компаний-партнеров Apple Pay.

Оплачивать услуги можно легко и просто

Оплачивать услуги можно легко и просто

В целом, пользователь приложения может без лишних проблем и задержек оплатить следующие товары и услуги:

- Такси;

- Еду в ресторане;

- Концертные билеты;

- Книги в электронном виде;

- Туристические поездки;

- Кофе в терминале самообслуживания;

- Продукты и бытовую химию в магазинах и гипермаркетах;

- Косметику;

- Одежду и многое другое.

Иными словами, купить при помощи приложения можно абсолютно любые товары и услуги в торговых точках, где принимают платеж данным способом, а также оплатить нужные предметы и товары в сети Интернет при совершении онлайн-покупок.

Digital wallet comparison

Here’s a comparison of Apple Pay, Google Pay and Samsung Pay.

| Digital wallet | Number of users | Pros | Cons |

| Apple Pay | 43.9 million |

|

|

| Google Pay | 25 million |

|

|

| Samsung Pay | 16.3 million |

|

|